How to prevent a housing crisis

Spiralling housing costs are causing despair across the EU. The situation is making people anxious that they will lose their accommodation or become homeless; they may become overburdened financially or forced to live in substandard accommodation; and many young people are unable to leave home. While renters in the private market have faced the largest cost increases and experienced the most problems with quality of accommodation, people with other types of housing tenure are in difficulty as well. Policy actions in line with the European Pillar of Social Rights and availing of Recovery and Resilience Facility (RRF) funds could both address and prevent problems.

Problem for renters and homeowners alike

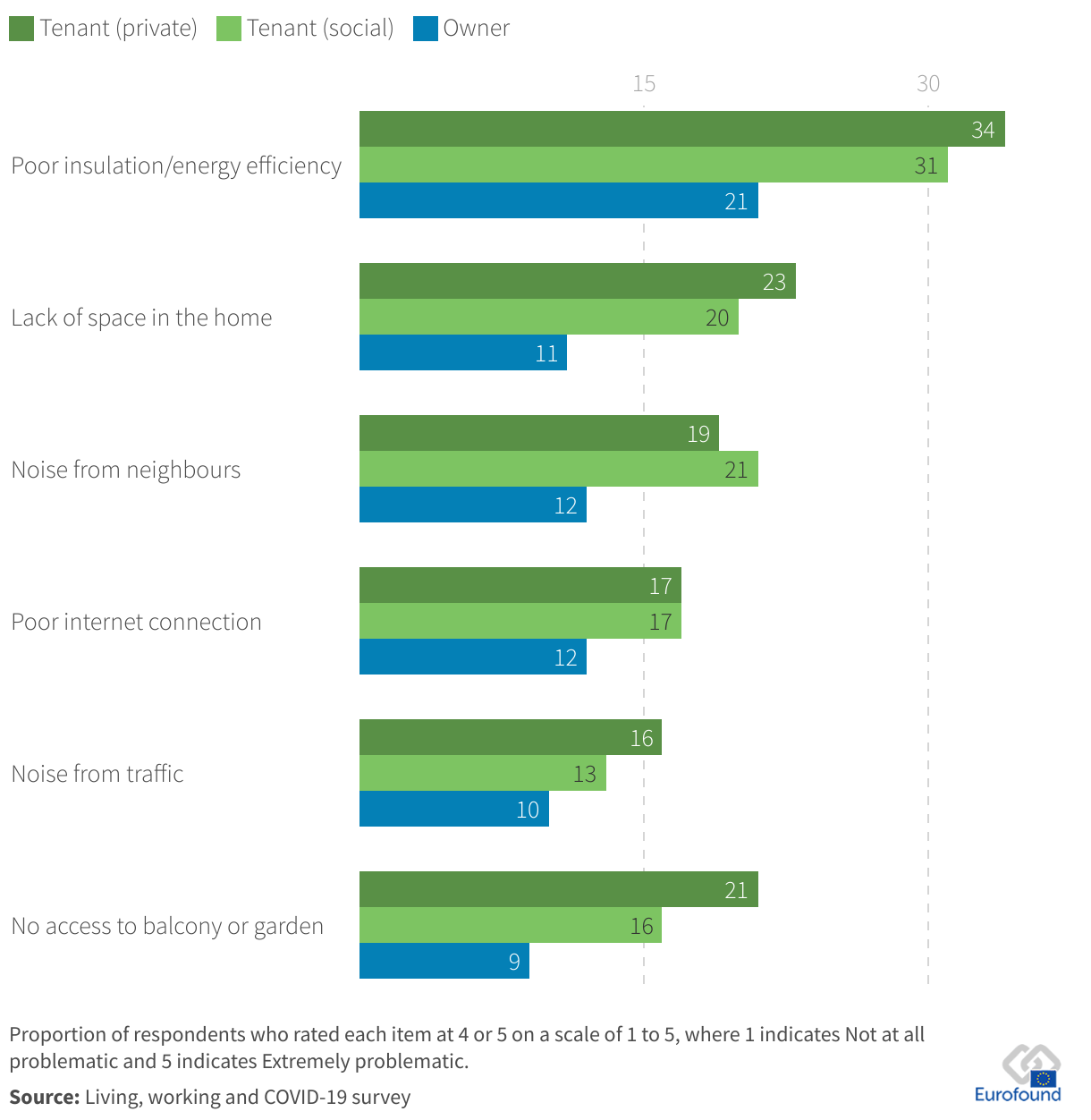

Renters have faced rapidly increasing housing costs over the past decade, while homeowners have seen their housing costs decline. Renters in the private market particularly are experiencing housing insecurity, with 46% saying they may have to leave their accommodation in the next three months because they can no longer afford it. Private tenants report problems with the quality of their accommodation – such as poor energy efficiency and lack of space – to a greater degree than homeowners, especially, but also tenants of social housing (Figure 1).

Figure 1: People reporting problems with accommodation, by type of tenure, EU, 2022 (%)

Housing problems are not confined to private renters, however. Homeowners with variable-rate mortgages are having to deal with rapidly increasing interest rates and, more broadly, the rising cost of living. There is clear evidence of this in Poland, for example, where the Borrower’s Support Fund (an initiative to support mortgage holders with payment problems) has seen a surge in demand since interest rates began to rise. An economic downturn would put even more people at risk.

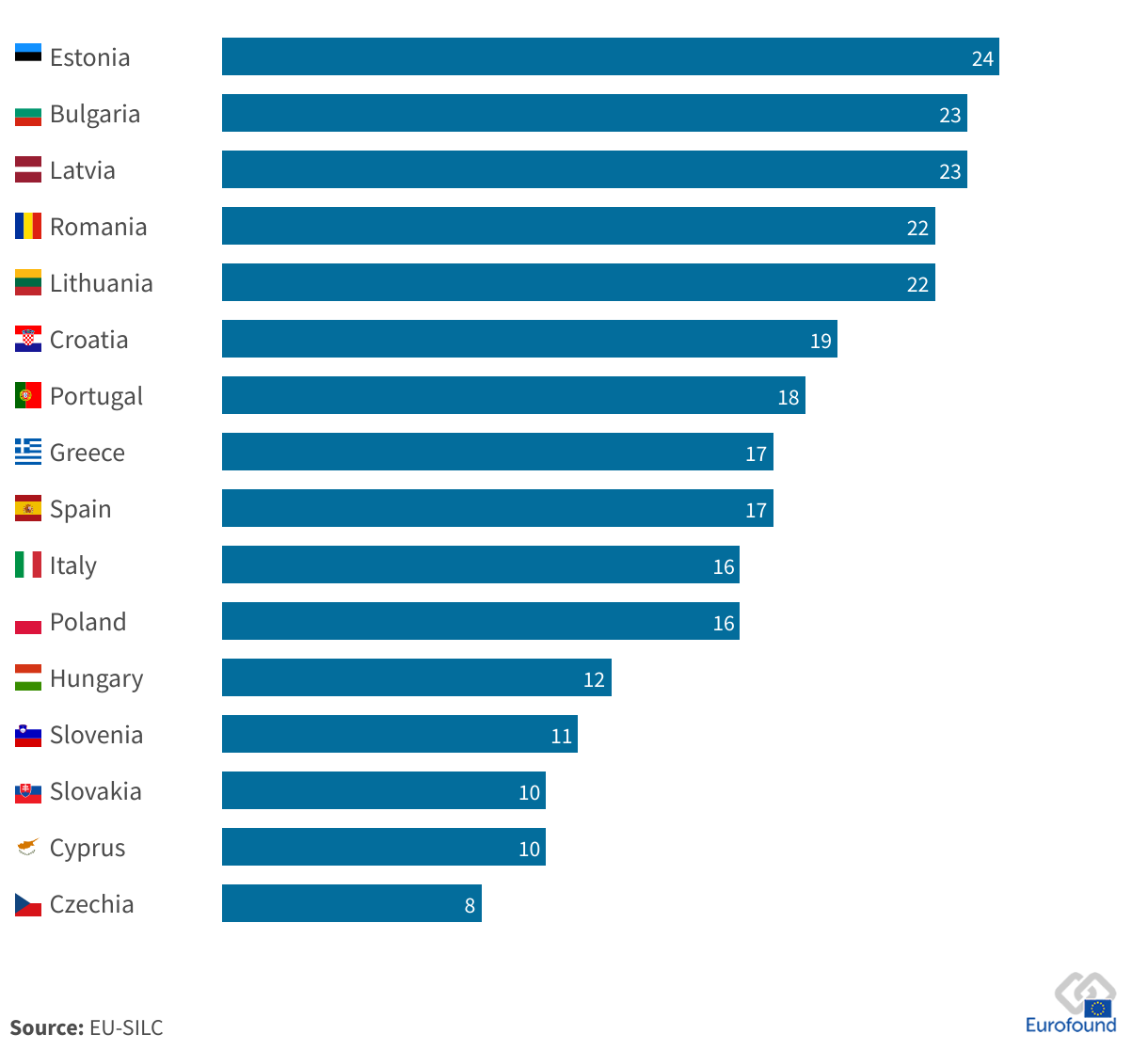

Even among people who own their home without a mortgage, many are struggling to pay for other housing-related costs such as utility bills. Figure 2 shows the 16 Member States with the highest rates of outright home ownership. As the graph illustrates, many of these outright owners are at risk of poverty: from 8% in Czechia up to 24% in Estonia. Furthermore, as an upcoming Eurofound report will reveal, many are unable to keep their homes at a suitable temperature due to poor energy efficiency and financial strain: at least 15% in Bulgaria, Cyprus, Greece, Lithuania and Portugal.

Figure 2: Risk of poverty rate among homeowners without a mortgage, in Member States with highest rates of ownership without a mortgage, 2020 (%)

Notes: The 16 Member States with the highest population percentages that own their home without a mortgage, varying from 38% in Portugal to 95% in Romania. Data for Italy is from 2019.

Compared with homeowners, tenants of social housing on average rate the quality of their accommodation lower and feel a higher degree of worry that they might be forced to leave their homes. They are more likely than private tenants to have difficulty paying for utilities. However, when comparing people with the same level of income, fewer social tenants than private tenants expect to have difficulty paying for utilities, implying that social housing contributes to protecting low-income groups against housing problems. Nevertheless, many do encounter difficulties with their homes, and the supply of social housing is limited in many Member States.

Unfortunately, homelessness is on the rise. While some countries have seen homelessness decrease (notably Finland), the problem is getting worse in others. In Ireland, for instance, the number of people accessing emergency accommodation has increased steadily from 7,991 in May 2021 to 11,754 in January 2023, with a risk of further increases now that the eviction ban has been lifted.

More generally, the winding down of cost-of-living support measures poses a risk for people who have depended on them.

What can policymakers do?

Housing support is a tricky area. Support for renting or purchasing housing, while important for many recipients, can drive up prices because it enables people to pay higher rents and purchase prices. Mortgage support tends to disproportionally benefit people with higher incomes, who are more likely to buy a home, and can cause people to get into excessive debt. In addition, many who are in need of support are not eligible. For example, those who are not entitled to rent benefits include: people without a fixed address; people in shared accommodation; migrants and mobile citizens; people with informal rental contracts; and people with low incomes just above the entitlement threshold. Others are entitled to housing benefits, but their right is not enforced – for instance, because they are unaware of it. People entitled to social housing often face difficulties accessing it, with Member States with both the largest and smallest social housing stocks having waiting lists.

Expanding the supply of quality housing plays an important role in putting downward pressure on rents and prices. Homes need to be built and renovated, while the practice of leaving accommodation vacant needs to be discouraged. However, it is not realistic to rely exclusively on increasing supply for a short- to medium-term solution, and the challenge needs to be addressed on several fronts simultaneously.

Detecting the early warning signs of payment problems so that personalised support can be triggered is fundamental. Sweden, for instance, requires planned evictions to be reported to a designated organisation, which then approaches the household and provides support to prevent eviction. Access to debt-settlement procedures and debt advice is also key, both for people with mortgage-payment problems and for people with accumulated rent or utility arrears. Ideally, though, support is set in motion earlier, for instance after a few months of missed utility bill, rent or mortgage payments.

Publication: Addressing household over-indebtedness

Payment problems and financial strain should, however, also be prevented rather than only addressed. There are different ways to do this. In relation to mortgages, policy needs to avoid facilitating take-up of large mortgages by people likely to encounter problems paying off their debts. Policymakers can also learn from Belgium, where most mortgage interest rates are fixed and where creditors are required to fund debt support, with contributions depending on the proportion of loans with arrears.

Regarding utility bills, more needs to be done to ensure that investments in improving energy efficiency, which the EU is funding massively through the RRF, reach low-income tenants and homeowners. This will protect households against energy price increases by decreasing their dependence on external energy, because they need less energy or generate their own.

Housing support should not be seen as separate from other social benefits and services. General social protection, such as a minimum income, and good access to services such as education and healthcare can help maintain the living standards of people who do not have access to housing benefits yet who feel the pressure of high housing costs.

To guarantee access to accommodation, stable and independent housing should be provided to people who are homeless or about to become so. Housing First policies are effective in doing so, but they need to be scaled up. About three-quarters of Member States have such schemes in place, but few have the capacity to house more than 1% of homeless people in the country. Furthermore, many of these schemes do not offer housing to people who refuse service support or offer housing in shared accommodation, at odds with the ideas behind Housing First.

Overall, Europe’s current housing situation calls for rapid and effective implementation of the European Pillar of Social Rights. Obviously, the rights directly linked to housing play a key role here. But so will implementation of the right to access good quality services and the right to other forms of social protection – these will be key in preventing and addressing housing problems.

Further reading

Publication: Addressing household over-indebtedness

Working paper: Local area aspects of quality of life: An illustrated framework

Publication: Inadequate housing in Europe: Costs and consequences

Publication: Access to social benefits: reducing non-take-up

Image © Onzeg/Adobe Stock

Author

Hans Dubois

Senior research managerHans Dubois is a senior research manager in the Social Policies unit at Eurofound. His research topics include housing, over-indebtedness, healthcare, long-term care, social benefits, retirement, and quality of life in the local area. Prior to joining Eurofound, he was Assistant Professor at Kozminski University (Warsaw). He completed a PhD in Business Administration and Management at Bocconi University (Milan), after working as a research officer at the European Observatory on Health Systems and Policies (Madrid).

Related content

31 May 2023