Employment in the EU’s automotive sector - Briefing note

PDF document

Δημοσιεύθηκε: 27 January 2025

In 2024, the automotive sector in the EU came to the fore in public and policy discussions. The focus was on the slowdown in electric vehicle (EV) sales, rising global competition, belated investments in new technologies, and the potential closure of production lines in Europe. A number of European car manufacturers and suppliers announced their intention to make large-scale redundancies and change long-standing collective agreements on job security and wages, while workers raised concerns amid demonstrations and industrial action.

This Eurofound briefing note provides more information on the latest EU employment statistics and the emerging data from the European Restructuring Monitor (ERM). It focuses on the core of the sector: NACE C29 (Manufacture of motor vehicles, trailers and semi-trailers) and G45 (Wholesale and retail trade and repair of motor vehicles). A Eurofound study on the impact of the twin transition on the automotive sector was published in December 2025.

The most recent key figures for the sector, published in the ACEA automobile industry guide for 2024/2025(opens in new tab)This link opens in a new tab and highlighted by the European Parliament Research Service (EPRS)(opens in new tab)This link opens in a new tab paint a concerning picture in relation to demand for and sale of EVs, lack of infrastructure, and incoherent incentives for consumers. Policy thinkers have warned of the competitiveness issues within the sector: the Draghi report(opens in new tab)This link opens in a new tab cited the automotive sector as ‘a key example of lack of EU planning, applying a climate policy without an industrial policy’. Commission President von der Leyen announced that she will lead a strategic dialogue on the future of the car industry in the EU, which will bring together sector players(opens in new tab)This link opens in a new tab ‘to design solutions together as this industry goes through a deep and disruptive transition’. The European Parliament also highlighted the importance of addressing the restructuring challenge in a draft motion(opens in new tab)This link opens in a new tab for a resolution in October 2024.

In emphasising the importance of the sector for the EU’s economy, both direct and indirect employment in automotive manufacturing and downstream industries are highlighted: the Draghi report suggests that 13.8 million Europeans, or 6.1% of the total labour force, are employed in the sector at large.

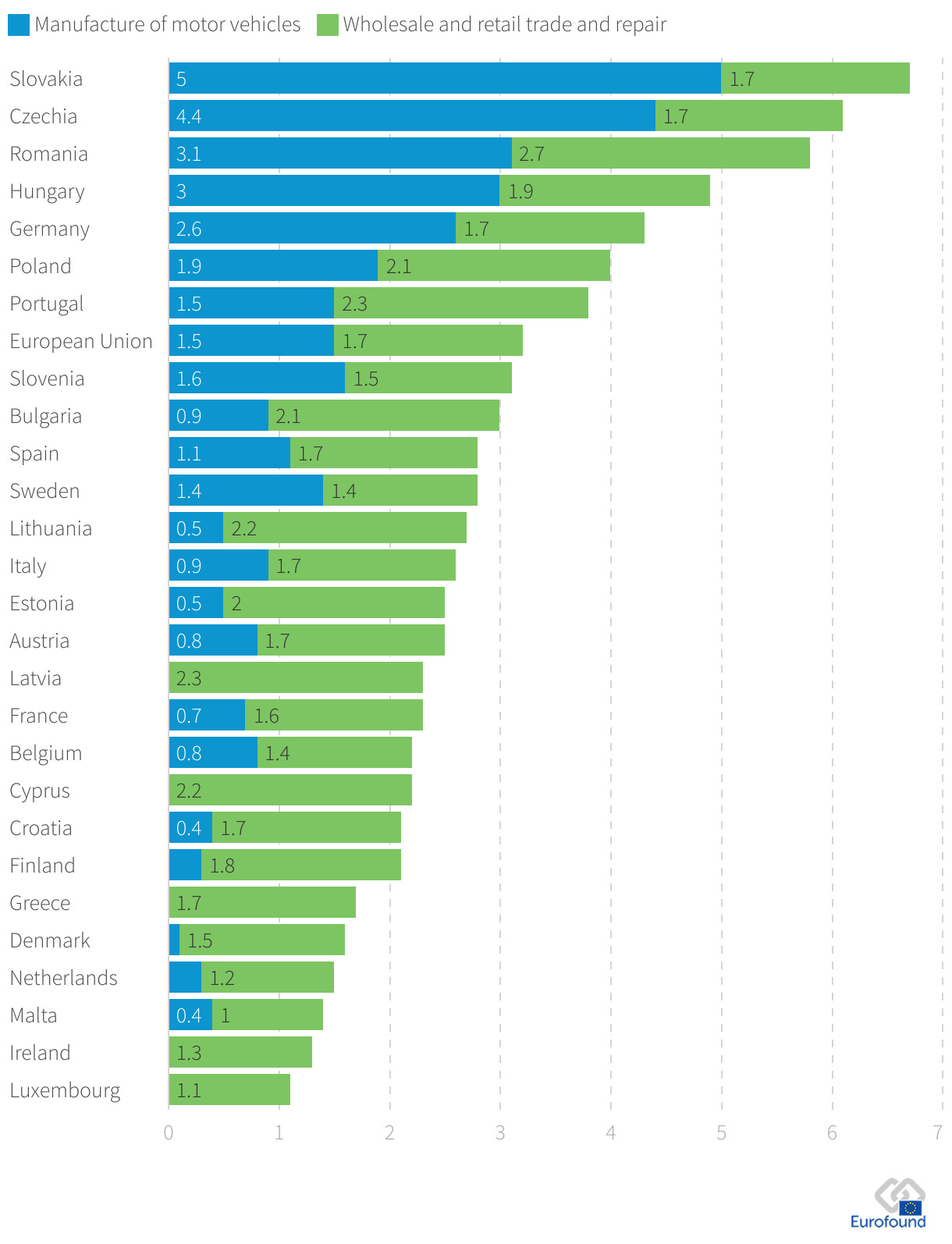

The latest EU Labour Force Survey data (EU-LFS) (Q3 2024) relating to the core subsectors show that there are 3.12 million jobs in motor vehicle manufacturing (C29) and 3.6 million jobs in sales and repairs (G45). With an estimated 6.72 million workers, these core elements of the automotive sector accounted for 3% of EU employment in Q3 2024. As a share of national employment, automotive manufacturing (C29) is highest in Slovakia, Czechia, Romania and Hungary, followed by Germany (Figure 1).

Figure 1: Employment in automotive sector by country, as a proportion of total employment, 2023 (%)

Source: EU-LFS

In the aftermath of the global financial crisis in 2007–2008, employment in vehicle manufacturing actually grew in the EU. This was in contrast to a secular trend in the overall labour market that saw a contraction in the manufacturing sector as a whole (in other words, a larger proportion of jobs were created in services). In more concrete terms, manufacturing as a whole in the EU shrunk by 0.6 percentage points, from 18.3% to 17.7% of total employment, between 2011 and 2022. This was in contrast, for example, to services in both the public and the private sector, which grew by more than 1 percentage point each over the same period (further information will be available in a forthcoming Eurofound report). The growth in employment in vehicle manufacturing was notable in both the European and the US economy. In the EU as a whole, there were 460,000 more jobs in vehicle manufacturing in 2024 compared with 2010, mostly due to growth in Czechia, Poland, Slovakia, Romania (Figure 2) and Sweden. In contrast, employment in automotive manufacturing has been falling in France over the last decade, and the decline has become more significant in Germany and Italy since 2019.

Employment levels in vehicle sales and repairs have been much more stable than those in automotive manufacturing (see Figures 2 and 3). In 2024, there were 120,000 more jobs in NACE G45 compared with 2010.

Employment contraction can co-exist with labour and skills shortages. According to the latest business and consumer survey data from Q4 2024, 13% of employers in the EU vehicle manufacturing sector indicated that labour was a factor limiting production – a year-on-year decline of 6 percentage points. This figure was highest in Poland at 45.1%. According to the World Economic Forum’s The Future of Jobs Report 2025(opens in new tab)This link opens in a new tab, global employers in the automotive and aerospace industry expect that there will be greater demand for robotics engineers, data analysts and AI and machine learning specialists, for example, while demand for assembly and factory workers and accounting professionals will tend to decline.

Figure 2: Employment trends in automotive manufacturing (C29), thousands

&w=3840&q=75)

Figure 3: Employment trends in automotive sales and repairs (G45), thousands

Notes: Due to a lack of data, the following countries are excluded from Figure 2: Cyprus, Estonia, Latvia, Luxembourg, Malta. The countries included in the geographical aggregates are Austria, Belgium, Denmark, Finland, France, Greece, Ireland, Italy, Luxembourg, Netherlands, Portugal, Spain and Sweden (‘western Europe’) and Bulgaria, Croatia, Cyprus, Czechia, Estonia, Hungary, Latvia, Lithuania, Malta, Poland, Romania, Slovakia and Slovenia (‘eastern Europe’).

Source: EU-LFS, 4Q moving average

Regardless of the overall trend towards the contraction of employment in manufacturing, the automotive sector has stood strong over the last 15 years in terms of jobs and quality of employment. Some of the key features of automotive manufacturing (C29) in the EU are listed below.

In the EU’s automotive manufacturing sector, 45% of the workforce are employed in the manufacture of motor vehicles (NACE 29.1); the remaining 55% are in the supplier industries.

Most employment in the sector is in large enterprises: 98% of the workforce in NACE 29.1 is employed in large enterprises with over 8,700 employees per enterprise on average. Around 17% of the labour force working in the supplier industry (NACE 29.3) are employed by small and medium-sized enterprises (SMEs). However, the remaining 83% of workers in the supplier industry are employed in large enterprises, each of which have on average 1,100 employees (Eurostat [sbs_sc_ovw]).

There is relatively high collective bargaining coverage in the sector as evidenced by Eurofound’s representativeness study on the metal sector.

Broadly compared with other sectors in the economy, wages are relatively high in the automotive sector. By the end of 2024, wage trends had diversified within the sector: an agreement(opens in new tab)This link opens in a new tab was reached to increase wages in a substantive share of the metal sector in Germany, including in some enterprises in the automotive industry. However, in some businesses, wages were part of a compromise to safeguard jobs.

There is a high rate of industrial and service robot usage: 36% of enterprises in automotive manufacturing, compared with 6% of all EU enterprises, use such robots (this refers to enterprises with 10 or more employees) (Eurostat [isoc_eb_p3dn2]). However, country differences are large. According to the International Federation of Robotics, around 1,500 robots per 10,000 employees were in operation in the automotive industry in Germany in 2023, while the rate in Poland was six times lower. In France, fewer than 1,000 robots were deployed in the sector; in Spain, the figure was close to 900. In Italy, Czechia and Slovakia, fewer than 700 robots per 10,000 employees were used in 2023. Over the last decade, the prevalence of automation in the automotive industry has been rising substantially in Czechia, Slovakia and Hungary, while in Italy and Spain there has been little change in recent years. For more information on the use of robots in the sector on a country-by-country basis, please see the data in Eurofound’s data catalogue.

Until recently, most of these features could have been considered to be strengths of the sector. However, as seen in the recent restructuring trends, the current headwinds are shaking up the entire car industry.

The overall trend in large-scale restructuring across the EU economy suggests that the extraordinary growth in employment that was a feature of the last few years is slowing down: data from Eurofound’s European Restructuring Monitor show that the number of jobs created and the number of jobs cut in large-scale restructuring in the EU have reached an equilibrium, with a tendency for increasing job cut announcements towards the end of 2024. The negative trend is much more visible in the automotive sector (Figure 4).

Figure 4: Restructuring announcements in EU’s automotive manufacturing – expected net employment change

Notes: EU-27; NACE C29, 4-month moving average. Data valid as of 13 January 2025. The ERM captures announcements of restructuring affecting at least 100 jobs or 10% of workers in enterprises with 250 or more employees, and may not reflect incremental employment changes and developments in SMEs.

Source: ERM

In 2024, announcements of large-scale restructuring in the automotive industry were made in most EU Member States. This mostly concerned job contraction: announcements made in 2024 suggested a forthcoming net loss of 53,669 jobs in the EU, or 88,669 jobs if Volkswagen’s announcement of 20 December 2024 is included (Table 1). Most companies mentioned rising costs, competitive pressure, the need to adapt sites to EV manufacturing and declining domestic and international demand as the reasons for the job cuts. Among the 104 restructuring announcements in the automotive sector in 2024, 10 concerned offshoring (moving a company’s activities to another country), mostly to or between eastern Member States and neighbouring countries in the Western Balkans; this accounted for 5,358 jobs destined to ‘leave’ their country, 3,610 of them were to be offshored beyond the EU.

The restructuring trends to watch are those that involve mergers, offshoring and reshoring, as well as those that entail adapting the existing manufacturing entities to EV-related production versus the establishment of separate businesses for such production.

At European level, the debate on factors affecting the sector has also alluded to climate-related policies and their potential impact on the cost of doing business; regulatory incentives for potential fleet renewal and technological upgrading (e.g. the EURO 7 standard, which sets out rules for emission limits and battery capacity); changing demand; and the need for measures to support workers and businesses during the just transition.

Table 1: Restructuring in the automotive sector – announcements and expected employment change, 2024

Notes: Data cover the countries in which restructuring events took place between 1 January 2024 and 1 January 2025, NACE C29 and G45. The ERM captures announcements of restructuring that affects at least 100 jobs or 10% of workers in enterprises with 250 or more employees, and may not reflect incremental employment changes and developments in SMEs.

Source: ERM

Bucking the trend in 2024, there was a net job increase in the automotive sector in Hungary and Spain. A number of companies expanded business in automotive manufacturing in 2024. Renault(opens in new tab)This link opens in a new tab and Ebro(opens in new tab)This link opens in a new tab both expanded capacity in Spain (500 and 607 jobs, respectively); Renault ElectriCity(opens in new tab)This link opens in a new tab recruited staff to prepare the E-Tech line in France (750 jobs). The German automotive industry supplier Kirchhoff(opens in new tab)This link opens in a new tab increased its production capacity in Hungary (100 jobs). According to ERM data, 5,978 new jobs were created in the EU’s automotive sector, via 18 cases of business expansion in 2024. Almost a third of these jobs (1,918) were a result of business expansion by Chinese companies (Eve Power(opens in new tab)This link opens in a new tab, ZS Europe(opens in new tab)This link opens in a new tab, Ebro(opens in new tab)This link opens in a new tab) and an American-Singapore company (Flextronics International Termelő és Szolgáltat(opens in new tab)This link opens in a new tab).

Some expansion in sectors outside of NACE C29 and G45 were also directly related to automotive manufacturing, such as Meta Systems(opens in new tab)This link opens in a new tab and Minebea Mitsumi's(opens in new tab)This link opens in a new tab growth in Hungary (494 and 200 jobs, respectively). Constellation(opens in new tab)This link opens in a new tab established a tech hub in Portugal for innovating in the automotive sector (100 jobs). Also of interest in terms of employing automotive manufacturing capacity was Milrem Robotics'(opens in new tab)This link opens in a new tab new set-up for military vehicles in Estonia (100 jobs).

The existing social partner agreements are a mediating factor that help companies adjust employment while changing the volume of production. Towards the end of 2024, social partner agreements were revisited by such major manufacturers as Volkswagen (see below) and Renault(opens in new tab)This link opens in a new tab. Specific employment effects included job losses in several countries in plants operated by the automotive manufacturer Stellantis and further stoppages in production in their plants in Italy at the end of 2024. Short-time working arrangements were reportedly put in place by Ford(opens in new tab)This link opens in a new tab in Cologne, and job cuts were subsequently announced in Germany and the UK in 2025. Slowing demand has also led to job cut announcements by suppliers such as Bosch(opens in new tab)This link opens in a new tab.

While the media disseminated news about Volkswagen, announcing the closure of some of its German factories, the actual timing of and severance payments for the closures are an object for social partner negotiation. Part of the 30-year collective agreement between the IG Metall union and employers was a ‘job guarantee’ covering 125,000 employees in Germany, which Volkswagen formally stepped away from in early September 2024 (alongside other agreements). This meant that the job guarantee would expire by the end of the year and that layoffs were technically possible by mid-2025 – if the conditions for issues such as number of jobs affected, severance payments and the like were agreed by the social partners by then. Strikes in Germany and the intensive negotiations that followed led to the conclusion of a social partner agreement at the end of December 2024. Entitled ‘Zukunft Volkswagen(opens in new tab)This link opens in a new tab’(Future Volkswagen), this agreement includes plans for the ‘socially responsible reduction of the workforce by more than 35,000 across Volkswagen’s German locations by 2030’ and a newly formulated job security plan up to 2030.

There are several key players in the industrial relations landscape in the sector – they include Ceemet (employer organisation) and industriAll Europe (trade union), which cover the metal sector. They are the recognised social partners working closely in the relevant EU-level social dialogue committee(opens in new tab)This link opens in a new tab. Associations such as ACEA and CLEPA represent automotive manufacturers and suppliers, while CECRA and ETRMA represent various subsectors and adjacent industries and their labour forces, such as those involved in supply chains for EVs; some segments of the sector are yet to develop social dialogue arrangements, as has been noted in the case of growing battery production in Hungary(opens in new tab)This link opens in a new tab, for example. These actors search for ways in which the industry can adapt; for example, they highlight the potential of the automotive electronics and semiconductor ecosystem(opens in new tab)This link opens in a new tab (CLEPA). In addition to industrial bodies, the Automotive Skills Alliance(opens in new tab)This link opens in a new tab is a partnership that involves regional authorities. Specific initiatives by companies or local authorities are also showcased within the framework of the European Commission-led Mobility Transition Pathway(opens in new tab)This link opens in a new tab, where examples of measures in the areas of automotive innovation, the future of the workforce, and the sustainability and competitiveness of the sector can be found. As part of this initiative, public and private stakeholders are called upon to make ‘pledges’ to encourage a green and digital transition. A new call for pledges runs until 28 February 2025.

A number of actions could be considered in order to effectively anticipate and address further change in the sector.

Guide the restructuring with regard to funding, training, re-skilling and job-to-job transitions.

The EU has experience in using tools such as the European Globalisation Adjustment Fund (EGF), which supports workers who have been displaced as a result of restructuring. Among the 69 applications(opens in new tab)This link opens in a new tab that have been filed with the EGF since 2014, 8 were to support displaced workers in the automotive industry. Approximately €32.8 million were granted in contributions from the EGF to support a total of 11,069 workers. The most recent EGF cases concern the closure of Nissan’s plant in Spain (2021) and offshoring of Van Hool production from Belgium (2024).

However, the EGF is currently limited in that it can only be applied after the event; in some cases, national instruments are more useful as they can be activated more rapidly. In addition, pre-emptive instruments that promote training and upskilling, for example, could be included in policymaking to address the issue of rising restructuring in the sector.

In the event of further employment contraction in the automotive sector, public policies, including EU support, could play a role in guiding the restructuring and job transitions. The sector’s needs could be raised in the context of EU initiatives, including the EU Talent Pool, the forthcoming Union of Skills and the Clean Industrial Deal.

Respond to labour shortages and direct labour supply towards the EU’s industrial priorities. Anticipatory policymaking could redirect the labour force to where it is badly needed before the situation exacerbates.

Policymaking could assist the sectors affected by persistent labour shortages, including those within the automotive sector.

Policies could be enacted to reskill highly skilled automotive workers for growing sectors, such as defence and infrastructure for EVs.

Prepare for future technologies.

Promote technological advancement: The impressive robotisation rate in the automotive industry in Germany was not enough to provide it with sufficient competitive advantage; in fact, the Draghi report calls for more automation.

Build on the sector’s labour force: The sector has a skilled workforce that has the ability to engage in training. This could facilitate the rapid take-up of new skills if new technologies emerge. It should be noted, however, that the shift towards more software-related and electric engineering skills may require effort. Assessing the skills potential could be among the forward-looking measures.

Contact: Tadas.Leoncikas@eurofound.europa.eu

With thanks to Delphine Rudelly (Ceemet) and Benjamin Denis (industriAll Europe) for their feedback.

Image © FotoArtist/Adobe Stock

Το Eurofound συνιστά την παραπομπή σε αυτή τη δημοσίευση με τον ακόλουθο τρόπο.

Eurofound (2025), Employment in the EU’s automotive sector, article.

All official European Union website addresses are in the europa.eu domain.

See all EU institutions and bodies

2 December 2025